Production of a comparison table for the budget expense line item 'Maintenance Materials' has yielded some disturbing results. The ability to clearly compare specific line items for each years budget against previous years figures, shows a need for the Operator/Management to explain or justify these huge increases to the residents budget.

Note: The figures put forward in the tables below are sourced from both the 'Proposed Budget' and the 'Income and Expenditure Statement' distributed by the Operator for each financial year. In other words, the figures displayed are all supplied by the Operator.

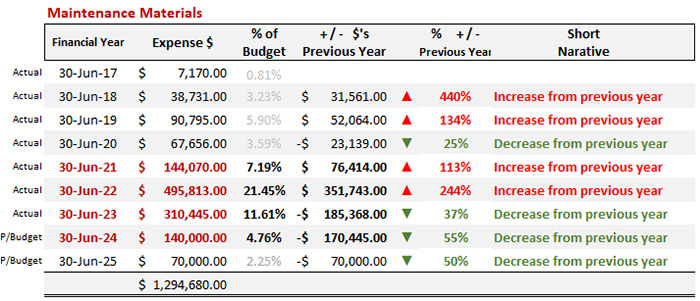

An examination of the graphic above, specifically the year ending 30 June 2022, the Operator has allocated $495,813 to the expenditure line item 'Maintenance Materials'. This amount, a tad under half a million dollars makes up just over 21% of the total expenditure for 21-22 residents budget.

Compare this to the 2019-20 budget, the same expense line item accounted for 3.59% of the total residents budget. In the 2020-21 budget, the same expense line item accounted for 7.19% of the total residents budget.

Even more concerning, the combined total of the 'Maintenance Material' line item for the previous 5 years, from 2017 to 2021 inclusive, was $348,422 - which is still $144,391 short of the half a million dollars, that the Operator allocated to the residents budget for 2021-2022.

Residents may well ask, what where the major projects and/or issues occuring within the village at that time, that required the Operator to purchase half a million dollars of materials and then allocate those expenses to the residents budget?

Major issues within the village

The 2021-22 Residents Committee had met with the Operator to clarify who was paying for several major projects undertaken by the Operator during the 2021-22 financial year.

The Operator was asked: -

- Who was paying for the stage 1 roof repairs? Operator answer. I am.

- Who was paying for the knock down and rebuild of the garden beds in Whaling Street? Operator answer. I am.

- Who was paying for the repairs to the water ingress issues of the villas? Operator answer. I am.

As the Operator had provided assurances that he was paying for the above mentioned issues, and the golf course was closed and certainly not functional at that time, what where the other major maintenance issues within the village that required resources (maintenance materials) to the value of $495,000. Certainly, none that the 2021 Residents' Committee was aware, that would go close to providing the Operator with a legitimate excuse to charge expenses against the Residents Budget Line Item 'Maintenance Materials' to the value of half a million dollars.

Editor's Note: As is evident from the above table, the Operator has spent almost half a million dollars on the cost of maintenance materials alone for the 2021-22 financial year. The above figures do not include any labour component.

Justified Concern

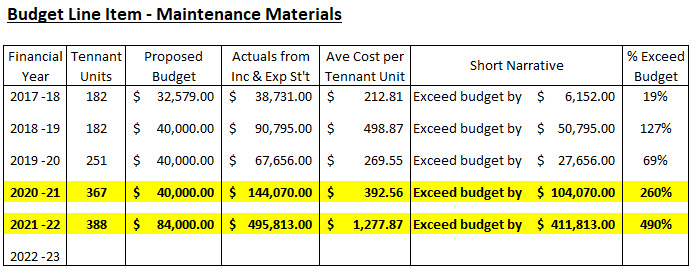

When residents examine the table (Graphic 1) above, it would be no surprise that the 2021-22 Residents Committee and Finance Sub-Committee were concerned about the meteoric rise of the Budget Line Item 'Maintenance Materials', over the 2020-21 and 2021-22 financial years, highlighted in yellow in the above table (Graphic 2).

Residents Committee request to sight associated invoices - Operator refused

The Residents Committee asked Management to produce the invoices for 'Maintenance Materials' for the 2021-22 financial year. This would enable the committee to personally examine the invoices to ensure that these huge expenses were justified in being part of the residents' budget, and secondly to ensure that such expenses had not been inadvertently or mistakenly allocated to the residents 'Material Maintenance' account in error.

Management's refusal to produce invoices, indicating 'Not entitled to see them'

The Operator granted the committee access to his Accountant in an effort to resolve the issue. On the pre-arranged day of the meeting, the Residents Committee, who had earlier contacted PKF(NS) Tax P/L requesting they bring the invoices for examination, failed to produce a single invoice at the meeting.

PKF(NS) Tax P/L insisted that their accounting system was both robust and accurate. Ms. Jennifer Stuart Smith further stated to the two committee members present at the arranged meeting, "You're not entitled to see the invoices".

Legal advice obtained

Residents may remember the Residents Committee had sought legal advice from Mr. Peter Hill, an RVRA recommended Solicitor, who in this matter, advised that the Residents Committee were entitled to see such invoices and if the committee required copies of said invoices, the Operator would be entitled to charge a nominal fee for providing same. The committee was happy to pay the nominal fee to examine and/or obtain copies of the invoices.

Logical assumption

If the Operator's accounting system is so robust and accurate, with all expenses checked, to ensure they have been allocated to the correct expense account, then why the reluctance to produce the invoices, which would allow the Residents Committee to see firsthand that the allocation of 'Maintenance Materials' expenses have been processed correctly.

![]() The Operator/Managements refusal to allow this examination, simply raises more red flags.

The Operator/Managements refusal to allow this examination, simply raises more red flags.

If the Residents Committee did not query a budget item that exceeded the proposed budget by more than $400,000 in a 12-month period, the residents of the village would be entitled to describe the committee as negligent in their duties.

The matter remains unresolved.