The Operator has provided limited or no financial reporting of money going out of the Capital Works Fund (CWF) in his 2020 - 2022 EOFY reports to residents.

There are no other transaction details, or reports presented to the residents of the village, which show the Operator has legitimately accessed and used money from the CWF or has been provided with approvals on expenditure allocated to the Capital Works Fund.

While this limited and one-sided form of reporting may be sufficient for the residents, if the Operator has not allocated expenses against the CWF in a given financial year, it is certainly not an acceptable form of financial reporting when the Operator has allocated expenses against the CWF, in that same year.

This type of limited financial reporting prevents residents from seeing the full extent of the activities revolving around the CWF.

How can the residents, the Residents Committee or the Finance Sub-Committe check the CWF account to ensure that their 'Capital Works Fund Contributions', any 'surplus to budget' amounts deposited as voted by residents, and/or any expenses allocated against (withdrawn from) the CWF, have been processed and accounted for correctly.

This would be like individual residents receiving a monthly bank statement for their credit card, showing only the deposits they've made into the account for the month, and then showing a closing balance. Without showing the other side of the equation, as in all the expenses or purchases they've made for that month, certainly provides a limited or one-sided picture to the credit card owner. It appears to be a very similar scenario with the CWF.

Editor's Note: The residents are entitled to see what money has gone into the capital works fund and what money has gone out of the capital works fund. A short transaction history is required each year for the capital works fund, so all residents can see how their money is being allocated and accounted for. The closing balance of the capital works fund should be in alignment with the end of financial year bank statement for the capital works fund account. These reports should be provided by management as part of the end of year financial reporting to residents.

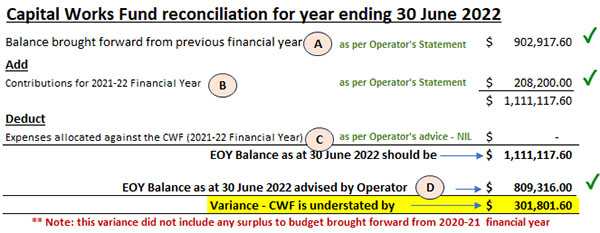

A good example of why this should occur is set out below:

As residents can easily see there is a substantial variation, exceeding $300,000, to the balance of the Capital Works Fund (CWF) as at the end of the 2021-22 financial year, put forward by the Operator/Management and the figures and subsequent calculations displayed above.

As the Operator/Management did not provide a single financial document or advice in the 2020-22 financial years, to the residents or the Residents Commitee to indicate that any expenses had been approved and allocated against the Capital Works Fund, we could assume that there were no outgoing expenses, as displayed and labelled item 'C' in the above reconciliation.

The only logical explanation for such a huge discrepancy in the above reconciliation was that large expenses had been allocated to the CWF, with little or no notification being provided to residents or the Residents Committee at the time.

The Retirement Villages Act shows two ways the Operator can access the CWF: -

- The Operator can indicate his intention to carry out maintenance to capital items, that the residents are responsible for, by disclosing his intent in the proposed budget for that year, and that budget must be approved by the residents. No such intent was indicated in the 2020-22 proposed budgets.

To examine the 2020-21 proposed budget put forward by management, click here...

To examine the 2021-22 proposed budget put forward by management, click here... - If the Operator did not indicate any maintenance to items of capital in the proposed budgets, but still wanted to carry out some form of maintenance to items of capital, he would then have to seek consent from the resident body, calling a meeting of residents, explaining to residents the need for such maintenance and that such maintenance expenses are eligible to be allocated against the capital works fund. Such consent would be sort via a special resolution and of course a 75% majority of those that vote would be required.

Neither of the above two options occurred during the 2020-22 financial years.

This gives rise to some serious issues that require answers from the Operator/Management.

- Where did the Operator get approval to access the Capital Works Fund, if it wasn't via the proposed budgets or via the resident body's approval at a special meeting and by a special resolution? Did he in fact gain any approval from the resident body to access the CWF?

Correspondence issued to residents by Ms. Jennifer Stuart Smith indicated that there were various concessions granted to the Operator/Management of retirement villages because of Covid-19, by way of Ministerial Orders. Further insisting that all expenses allocated to the CWF were approved. While this information provided some insight as to Managements right to access the CWF, no definitive information, quoting which Ministerial Order they were reliant on, was forthcoming.

None the less, enquiries made with NSW Fair Trading, indicated that no additional relief has been provided by Ministerial Orders, to Operators of retirement villages to access 'Capital Works Funds', outside the two methods described above.

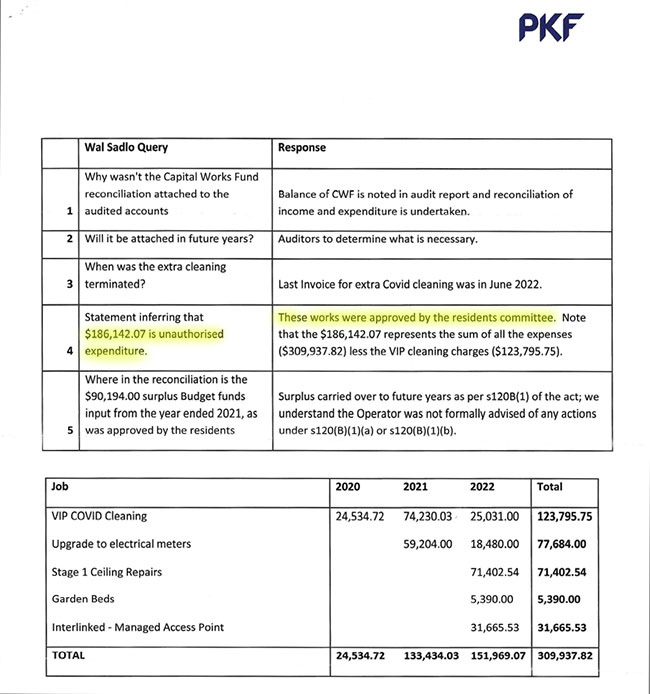

Thanks to Ms. Jennifer Stuart Smith, who was providing answers to a resident's enquiry into the discrepancy of the balance of the CWF, as indicated above, she provided a document from PKF(NS) Tax P/L, to support her assertion that all expenses allocated against the CWF were in fact, approved.

Set out below is a copy of that correspondence: -

It is thanks to this correspondence that we are now aware that the Operator had called a meeting or meetings with a member or members of the Residents Committee at the time, seeking approval to allocate large expenses against the CWF. According to the same correspondence, page 2 above, the Residents Committee members approved $186,142.07 of expenses to be allocated against our CWF.

While the above correspondence clearly indicates Mr. Singer and Mr. Porvaznik were in attendance at such meetings, it fails to identify those resident committee members, who provided such approvals.

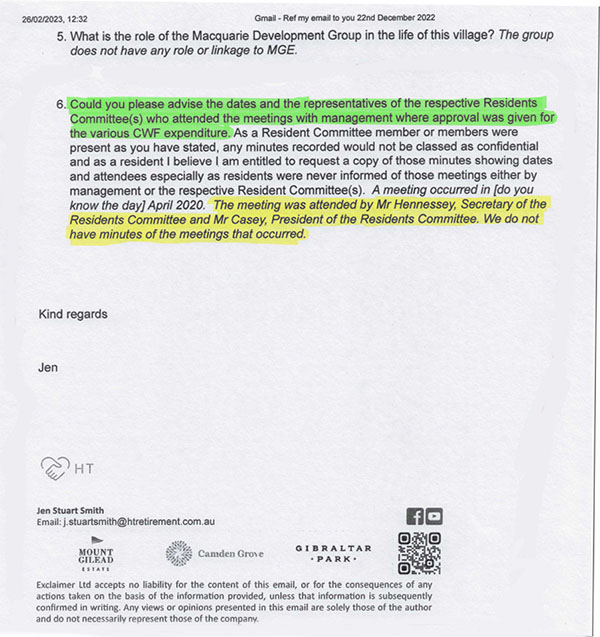

Our ever-intrepid resident, Mr. Walter Sadlo was determined to find out which resident committee members provided such approvals to the Operator.

Further email communications with Ms. Jennifer Stuart Smith, provided Mr. Sadlo with the following email response regarding this issue.

As the above information has been supplied by Ms. Jennifer Stuart Smith, in response to Mr. Sadlo's questions relating to the CWF, there can be little doubt as to how the Operator obtained approval for such large expenses to be allocated against our CWF.

A member or members of a residents committee do NOT have the authority to provide approval to the Operator to allocate large expenses against the CWF. Those committee members, Mr. Casey and Mr. Hennessey have certainly overstepped their authority.

A check of all correspondence from the Casey/Hennessey Residents Committee showed no advice was provided to residents about the approval/s provided to the Operator to access $186,142.07 of the CWF, nor was there any record of such meetings with the Operator, supported by resident committee minutes.

Ms. Stuart Smith also acknowledges that Management do NOT have minutes of the said meetings that occurred.

Examination of the CWF continues, but it is clear that the Operator/Management have not complied with the Retirement Villages Act in the manner they have accessed the CWF.

An examination of some of the expenses approved by Casey/Hennessey shows they have approved the purchase of new capital items, which should be at the Operators' expense and certainly not an expense that can be allocated against the CWF.

It is evident that this issue involves hundreds of thousands of dollars and is one that should be pursued by both the current Residents Committee and the current Auditor, Bishop Collins, as it has the propensity to save the residents of this village a very large sum of money.