Residents may remember at the 2022 Annual Management meeting, a resident, Mr Walter Sadlo, raised issues about the 'Capital Works Fund', to Jennifer Stuart Smith, Chair of the meeting and General Manager HTR.

In short, Mr. Sadlo expressed concerns that the current 'Capital Works Fund' balance appeared to be well short of calculations made, considering the previous year's balance, plus the inputs from the budget, and the fact that no reports had been disseminated by management or the residents committees in power at the time, that large expenses had been allocated against the resident's capital works fund (CWF). Could Ms. Stuart Smith provide an explanation.

Ms. Stuart Smith could not provide such details off the top of her head, and informed the residents that she would come back to them with an answer in seven days. Ms. Stuart Smith did not come back to the residents in her nominated time, and both Mr. Sadlo and the Residents Committee (including the Finance Sub Committee) had to chase her for more definitive information.

Using end of year balances for the Capital Works Fund supplied by Management, it became evident to Mr. Sadlo and the Finance Sub-Committee that there must have been large expenses allocated against the capital works fund, which would be the only logical explanation for such discrepancies in the balances for the CWF, put forward by management.

Mr. Sadlo had further communications with Ms. Stuart Smith, regarding this issue. Ms. Stuart Smith informed Mr. Sadlo that such expenses allocated against the capital works fund had all been approved.

Mr. Sadlo was aware that Management, and the Residents Committees in power at the time had not called a meeting of residents to seek approval, via a special resolution, to allocate expenses against our capital works fund (CWF). Further, he checked all communications from management and the residents' committees, and could find no communications from either, advising that large expenses had been approved, and allocated against the residents' capital works fund.

This prompted Mr. Sadlo to ask Ms. Stuart Smith, who approved such large expenses allocated against our capital works fund for the last couple of years?

In reply to Mr. Sadlo's questions, Ms. Jennifer Stuart Smith supplied the following information (letter). Ms. Stuart Smith freely provided this letter to Mr. Sadlo, in answer to his questions, about the CWF and the village finances. No restrictions, either verbally or in written form, were advised by Ms. Stuart Smith as to the supplied letters use. Mr. Sadlo provided this letter to the Residents Committee at the time, for the information and benefit of all residents and other interested parties.

From the attached letter (shown below) on PKF letterhead, it would appear that Jennifer Stuart Smith had sought information from PKF(NS) Tax P/L in answer to Mr. Sadlo's questions regarding the capital works fund, and this letter is in response to the information sought.

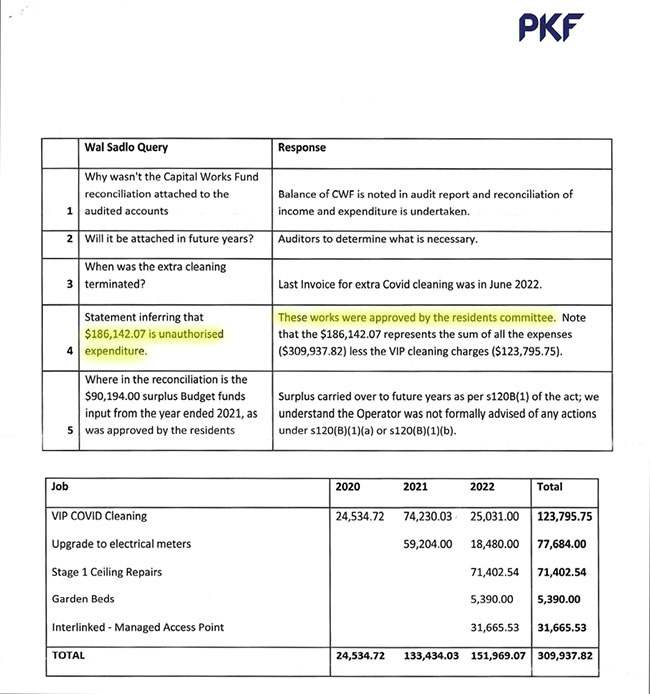

Page 1 of the letter dated 21 December 2022.

It is clear from the above correspondence that Mr. Porvaznik, Director of PKF(NS) Tax P/L, Paul Singer, and a member or members of the Residents Committee in power at the time, attended such meetings, where Management was seeking approval to allocate expenditure against the residents 'Capital Works Fund'.

Editor's Note: Resident Committe's do not possess the power or authority to approve requests from management to allocate expenses against the resident's capital works fund. That power remains with the residents of the village.

The actions by Mr. Singer, to call a meeting seeking approval from a member or members of the residents committee, for large expenses to be allocated against the capital works fund is indeed puzzling. The Retirement Villages Act 1999 (RV Act) is clear, the Operator and his employees are to be fully conversant and or educated in relation to the RV Act, by which they are governed.

As Mr. Singer has been acting as the Operator of the village for many years, it would be a reasonable assumption he would have an extensive knowledge of the RV Act and its Regs.

This gives rise to several questions which need to be put to Mr. Singer.

Q1. As Mr. Singer would be aware; a residents committee member, members or the whole committee, have no power or authority to approve expenses to be allocated against the resident's capital works fund. So why seek approval in such a manner?

Q2. One would assume both Mr. Singer and Mr. Porvaznik would be well aware of the parameters in which they should be operating, set out under the Retirement Villages Act and its Regs. Ministerial Orders as a result of the Covid 19 pandemic, did not provide relief to the Operator/Management of a retirement village to access the resident's capital works fund via approval from a member or members of a residents committee. At best, such approvals are unauthorized, and any expenses allocated against the resident's capital works fund in this manner, would be in breach of the RV Act. Is Mr. Singer prepared to reimburse the residents capital works fund for any and all expenses approved in this manner.

Additional information still required

While Mr. Porvasnik, Director of PKF(NS) Tax P/L, has made it abundantly clear that upper management of HTR were present at these meetings, he fails to name those residents committee members who attended and provided approval for the allocation of expenditure against the resident capital works fund.

So, there is one question remaining, who were the members of the residents' committee that have certainly overstepped their authority and provided such approvals?

Let's move to page 2 of the letter, supplied by Jennifer Stuart Smith.

Page 2 of the letter dated 21 December 2022.

Referencing item 4 in the table above - 'statement inferring that $186,147.07 is unauthorized expenditure. In the response column to the right, states - 'These works were approved by the Residents Committee. Note, that the $186,147.07 represents the sum of all the expenses ($309,937.82) less the VIP cleaning charges ($123,795.75)'.

If 'these works ($186,147.07)' were approved by a member or members of the Residents Committee at the time, and not previously mentioned, proposed and/or approved by the residents as part of the budget and proposed capital works expenditure for that year, then at the very least, such approvals are unauthorized and certainly in breach of the Retirement Villages Act.

An examination of all budgets from 2019 to 2023, shows no proposed capital works expenditure has been advised by management in any of the below mentioned budgets. These budgets are available for your examination below, simply follow the links provided.

- To see the proposed budget for the 2019-2020 budget year, click here.

- To see the proposed budget for the 2020-2021 budget year, click here.

- To see the proposed budget for the 2021-2022 budget year, click here.

- To see the proposed budget for the 2022-2023 budget year, click here.

If, as indicated by Mr. Porvaznik in his correspondence, the residents committee at the time had provided such approvals for $186,147.07 worth of expenses to be allocated against our capital works fund, then surely some advice from either the residents committee at the time and/or management would follow.

Search for Residents' Committe Minutes and or advice from Management

A search of all residents committee minutes could not find a single reference to such meetings with management and could not find any advice to residents of the village, that such large expenses had indeed been approved by the residents committee in power at the time, on behalf of the full resident body.

No meetings had been called by the Residents' Committee in power at the time, or by the Management, seeking permission via special resolution, to allocate expenses against our capital works fund. A requirement under the Retirement Villages Act. Mr. Porvaznik does indicate that 'there were various concessions granted during covid as meetings were not possible'. No further details on such concessions were mentioned or supplied.

We will come back to the concessions mentioned (Ministerial Orders), later in this article.

The question which remained unanswered - Which committee and which committee members attended these meetings and provided such approvals?

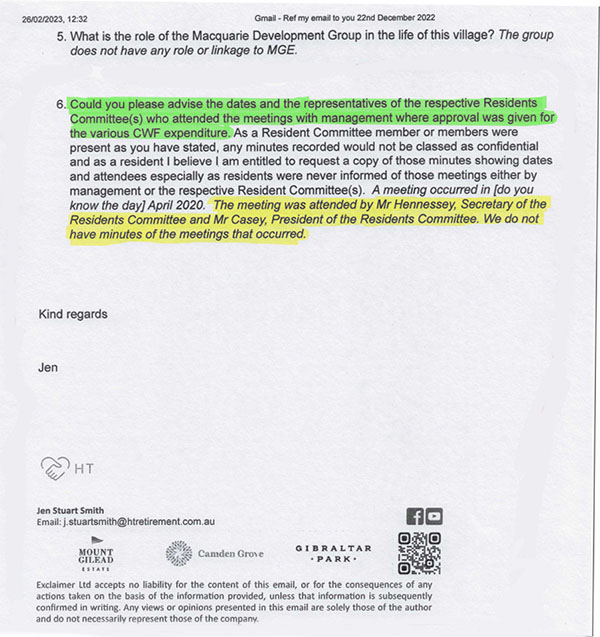

Mr. Sadlo sought this additional information from Ms. Jennifer Stuart Smith via Email correspondence. A part extract of the response email correspondence from Ms. Stuart Smith, dated 22 December 2022, is shown below: -

Ms. Stuart Smith's email response to Mr. Sadlo's questions, clearly indicating (highlighted in yellow above) that Mr. Casey and Mr. Hennessey were the two resident committee members, who attended the said meetings and provided such approvals to the Operator/Management to allocate thousands of dollars of expenses against our capital works fund.

Ms. Stuart Smith also states - 'We do not have minutes of the meetings that occurred'.

Why would management not minute a meeting specifically designed to seek approval for exceptionally large expenses to be allocated against our capital works fund? At the very least it appears to be poor work practice, involving large sums of money.

There are some significant questions to be asked in relation to this issue.

- Management has called a meeting with a member or members of the Residents' Committee at the time, seeking approval for $186,142.07 worth of expenses to be allocated against the resident's capital works fund, yet does not have minutes of such meeting/s. Why?

- Residents' Committee members at the time, (including the committee secretary, Hennessey) attended the meetings, provided approval for $186,142.07 worth of expenses to be allocated against the resident's capital works fund, yet they too, appear to have failed to minute and distribute any details of such meetings to the residents. Why?

- Another reasonable question to ask is why the Residents' Committee at the time failed to inform the residents of the village about the decision they have made on their behalf. Why?

- Where is Managements responsibility in this issue?

- If Management/Operator feels they have been provided some form of relief to obtain approval via a member or members of a resident committee to allocate expenses against the capital works fund, because of Ministerial Orders that were in force at the time, then management should produce such documentation in support of their actions.

To examine those expenses that were approved by Mr. Casey and Mr. Hennessey. Please click here....